Bank Sector Outlook 2019: End of the Great Australian Bank Sector Boom

The financials sector has typically provided strong dividend yields and formed a core part of Australian investor portfolios.

This is a summary of our research. Please click here to request the full report.

INTRODUCTION

The financials sector has typically provided strong dividend yields and formed a core part of Australian investor portfolios.

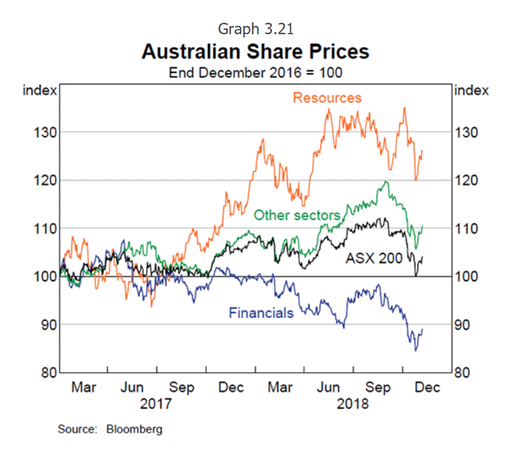

However, the sector has significantly underperformed the wider market through 2018. Given this, it is appropriate to analyse the 2019 sector outlook. Table 1 illustrates the extent of underperformance of the financials sector.

TABLE 1: AUSTRALIAN EQUITIES SECTOR PERFORMANCE

Source: RBA Quarterly Statement of Monetary Policy, Nov 2018

2019 OUTLOOK

Regulatory changes are likely to dominate newsflow in the near-term.

Whilst the Hayne Royal Commission has shone a light on the major banks’ unethical conduct and already adversely impacted share prices, there are still several risks yet to play out and potentially impact share prices. An incoming Shorten Labor Government could re-introduce sovereign risk to the sector, with potential changes to negative gearing likely to exacerbate a property market downturn and potential changes to dividend imputation likely to reduce banks’ yield support.

The bearish investment case is extensive including:

Royal Commission recommendations (Feb 2019),

Federal election and potential change of Government (~May 2019), including changes to franking credits and negative gearing, Slowing credit growth,

The structural impact of tighter lending and improved ethical behaviour resulting in lower loan volume, Margin pressure,

Rising interest rates,

The risk of an under-provisioned bank sector coming into a housing market slowdown and with significant interest only refinancings to principal & interest loans, and

Fintech disruption of staid, oligopolistic banking business models.

The bullish investment case is that current share prices already discount risks and offer attractive yields.

However, the yield support argument quickly diminishes if:

Dividends are cut,

Franking credits reduced, or

Investors simply seek yield in other parts of the market without such extensive downside risks.

We consider the valuation argument below.

VALUATION CONSIDERATIONS

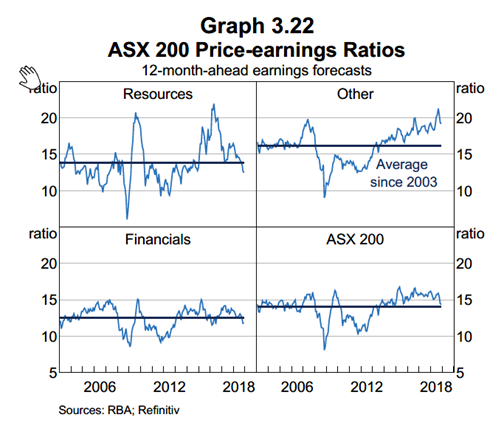

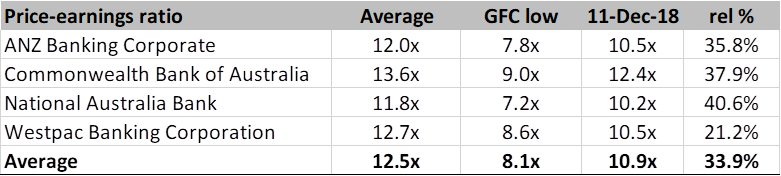

Tables 2 and 3 shows that major bank PE ratios could decline further.

Currently, the average of the 4 major banks PE ratios is 10.9x. This compares to the 8.2x bottom during the Global Financial Crisis. In other words, equity investors have applied a 34% lower PE valuation to the sector in previous years. Whilst we are not suggesting that 2019 will bring another GFC, we are highlighting that investors have marked down banks even more aggressively in previous years. “Cheap” bank stocks can become “cheaper” – ie. downside valuation risks remain.

TABLE 2: MAJOR BANK PRICE-EARNINGS RATIOS

Source: RBA Quarterly Statement of Monetary Policy, November 2018

TABLE 3: MAJOR BANK PRICE-EARNINGS RATIOS

Source: Bloomberg, Kennedy Partners

ASK THE ANALYST

Our analysts are ready to answer any questions you have

SECTOR PERFORMANCE CONSIDERATIONS

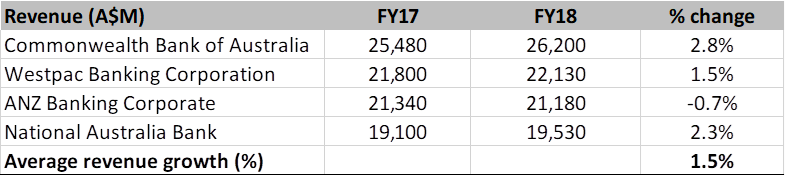

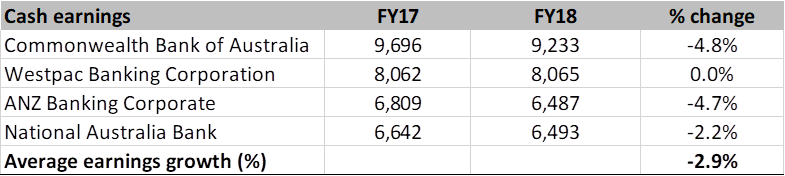

Recent results updates from the major banks highlight weak overall performance.

The sector’s average 1.5% revenue growth and -2.9% earnings growth does not augur well for the 2019 outlook as the sector confronts a number of structural and cyclical challenges. TABLE 4: MAJOR BANK REVENUE GROWTH TRENDS

TABLE 5: MAJOR BANK EARNINGS GROWTH TRENDS

CONCLUSION -SECTOR RISKS LIKELY TO OVERHANG 2019 OUTLOOK

Our investment view is to remain underweight the banks sector.

We will retain our underweight view until

A sustainable earnings base becomes visible,

Some regulatory clarity emerges and/or

Some of the broader risks have played out.

Bank share prices are unlikely to rally in the near-term as there is no clear driver of earnings growth across the 4 major banks for 2019. Most likely, the driver of share price recovery would be when investors feel they are able to look through the risks we have identified above. Earnings growth is not likely to drive major bank share price recovery for some time.

However, further earnings and valuation downside is possible as sector risks continue to play out through 2019.

FURTHER RESEARCH

For interested investors, we have undertaken further research in 6 Parts:

Part 1 – Sector Index weighting Part 2 – Key risks Part 3 – What will drive earnings growth? Part 4 – A scorecard: current sector performance Part 5 – Valuation considerations Part 6 – Key Conclusions

This is a summary of our research. Please click here to request the full report.

This document is provided by RP Investment Management Pty Ltd trading As Bletchley Park Capital AFSL 1267413 Corporate Authorised Representative of BR Securities Australia Pty Ltd. The material in this document may contain general advice or recommendations which, while believed to be accurate at the time of publication, are not appropriate for all persons or accounts.

Reach Markets Disclaimer

Reach Markets Pty Ltd (ABN 36 145 312 232) is a Corporate Authorised Representative of Reach Financial Group Pty Ltd (ABN 17 090 611 680) who holds Australian Financial Services Licence (AFSL) 333297. Please refer to our Financial Services Guide or you can request for a copy to be sent to you, by emailing [email protected]. The material in this document may contain general advice or recommendations which, while believed to be accurate at the time of publication, are not appropriate for all persons or accounts.

Read our full disclaimer here >

This publication contains general securities advice. In preparing the advice, Reach Markets Australia has not taken into account the investment objectives, financial situation and particular needs of any particular person. Before making an investment decision on the basis of this advice, you need to consider, with or without the assistance of a securities adviser, whether the advice in this publication is appropriate in light of your particular investment needs, objectives and financial situation. Reach Markets Australia and its associates within the meaning of the Corporations Act may hold securities in the companies referred to in this publication. Reach Markets Australia does, and seeks to do, business with companies that are the subject of its research reports. Reach Markets Australia believes that the advice and information herein is accurate and reliable, but no warranties of accuracy, reliability or completeness are given (except insofar as liability under any statute cannot be excluded). No responsibility for any errors or omissions or any negligence is accepted by Reach Markets Australia or any of its directors, employees or agents. This publication must not be distributed to retail investors outside of Australia. It is recommended that you seek independent advice and read the relevant Product Disclosure Statement before making a decision in relation to any investment. Any advice contained in this communication is general and has not taken into account the investment objectives, financial situation and particular needs of any particular person.

Recommendation Rating Guide

Recommendation Rating Guide

Total Return Expectations on a 12-mth view

Speculative Buy

Greater than +30%

Buy

Greater than +10%

Neutral

Greater than 0%

Sell

Less than -10%

Reach Markets Disclaimer

Reach Markets Pty Ltd (ABN 36 145 312 232) is a Corporate Authorised Representative of Reach Financial Group Pty Ltd (ABN 17 090 611 680) who holds Australian Financial Services Licence (AFSL) 333297. Please refer to our Financial Services Guide or you can request for a copy to be sent to you, by emailing [email protected].

Read our full disclaimer here >

This publication contains general securities advice. In preparing the advice, Reach Markets Australia has not taken into account the investment objectives, financial situation and particular needs of any particular person. Before making an investment decision on the basis of this advice, you need to consider, with or without the assistance of a securities adviser, whether the advice in this publication is appropriate in light of your particular investment needs, objectives and financial situation. Reach Markets Australia and its associates within the meaning of the Corporations Act may hold securities in the companies referred to in this publication. Reach Markets Australia does, and seeks to do, business with companies that are the subject of its research reports. Reach Markets Australia believes that the advice and information herein is accurate and reliable, but no warranties of accuracy, reliability or completeness are given (except insofar as liability under any statute cannot be excluded). No responsibility for any errors or omissions or any negligence is accepted by Reach Markets Australia or any of its directors, employees or agents. This publication must not be distributed to retail investors outside of Australia.

It is recommended that you seek independent advice and read the relevant Product Disclosure Statement before making a decision in relation to any investment. Any advice contained in this communication is general and has not taken into account the investment objectives, financial situation and particular needs of any particular person.

Banyan Tree Disclaimer

This document is provided by Banyan Tree Investment Group (ACN 611 390 615; AFSL 486279) (“Banyan Tree”).

The material in this document may contain general advice or recommendations which, while believed to be accurate at the time of publication, are not appropriate for all persons or accounts. This document does not purport to contain all the information that a prospective investor may require. The material contained in this document does not take into consideration an investor’s objectives, financial situation or needs. Before acting on the advice, investors should consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. The material contained in this document is for sales purposes. The material contained in this document is for information purposes only and is not an offer, solicitation or recommendation with respect to the subscription for, purchase or sale of securities or financial products and neither or anything in it shall form the basis of any contract or commitment. This document should not be regarded by recipients as a substitute for the exercise of their own judgment and recipients should seek independent advice.

The material in this document has been obtained from sources believed to be true but neither Banyan Tree nor its associates make any recommendation or warranty concerning the accuracy, or reliability or completeness of the information or the performance of the companies referred to in this document. Past performance is not indicative of future performance. Any opinions and or recommendations expressed in this material are subject to change without notice and Banyan Tree is not under any obligation to update or keep current the information contained herein. References made to third parties are based on information believed to be reliable but are not guaranteed as being accurate.

Banyan Tree and its respective officers may have an interest in the securities or derivatives of any entities referred to in this material. Banyan Tree does, and seeks to do, business with companies that are the subject of its research reports. The analyst(s) hereby certify that all the views expressed in this report accurately reflect their personal views about the subject investment theme and/or company securities.

Although every attempt has been made to verify the accuracy of the information contained in the document, liability for any errors or omissions (except any statutory liability which cannot be excluded) is specifically excluded by Banyan Tree, its associates, officers, directors, employees and agents. Except for any liability which cannot be excluded, Banyan Tree, its directors, employees and agents accept no liability or responsibility for any loss or damage of any kind, direct or indirect, arising out of the use of all or any part of this material. Recipients of this document agree in advance that Banyan Tree is not liable to recipients in any matters whatsoever otherwise recipients should disregard, destroy or delete this document. All information is correct at the time of publication. Banyan Tree does not guarantee reliability and accuracy of the material contained in this document and is not liable for any unintentional errors in the document.

The securities of any company(ies) mentioned in this document may not be eligible for sale in all jurisdictions or to all categories of investors. This document is provided to the recipient only and is not to be distributed to third parties without the prior consent of Banyan Tree.

This document has been commissioned by Reach Markets Australia Pty Ltd and provided by Banyan Tree Investment Group (ACN 611 390 615; AFSL 486279) (“Banyan Tree”).